Date published:15/04/2026

The UK private care home market is experiencing a widening gap between demand and deliverable supply. Demographic shifts are structurally increasing long-term demand. The UK is forecast to see its population aged over 80 double over the next 20 years.

Alongside rising life expectancy, the increased prevalence of chronic and complex health conditions is sustaining pressure on NHS capacity, reinforcing long-duration demand for private residential care. These demand dynamics have led investors – including some that have historically shied away from operational real estate – to gravitate to the sector’s deep structural demand.

But the ‘demand outstrips supply’ narrative is only half of a complex market structure. In practice, supply expansion has been constrained for years by cost inflation and regulatory constraints that undermine development viability. The national care home supply shortfall – relative to the UK’s ageing population – continues to widen as development and capital concentrate in more affluent, private-pay supported regions, leaving much of the broader market undersupplied and financially constrained.

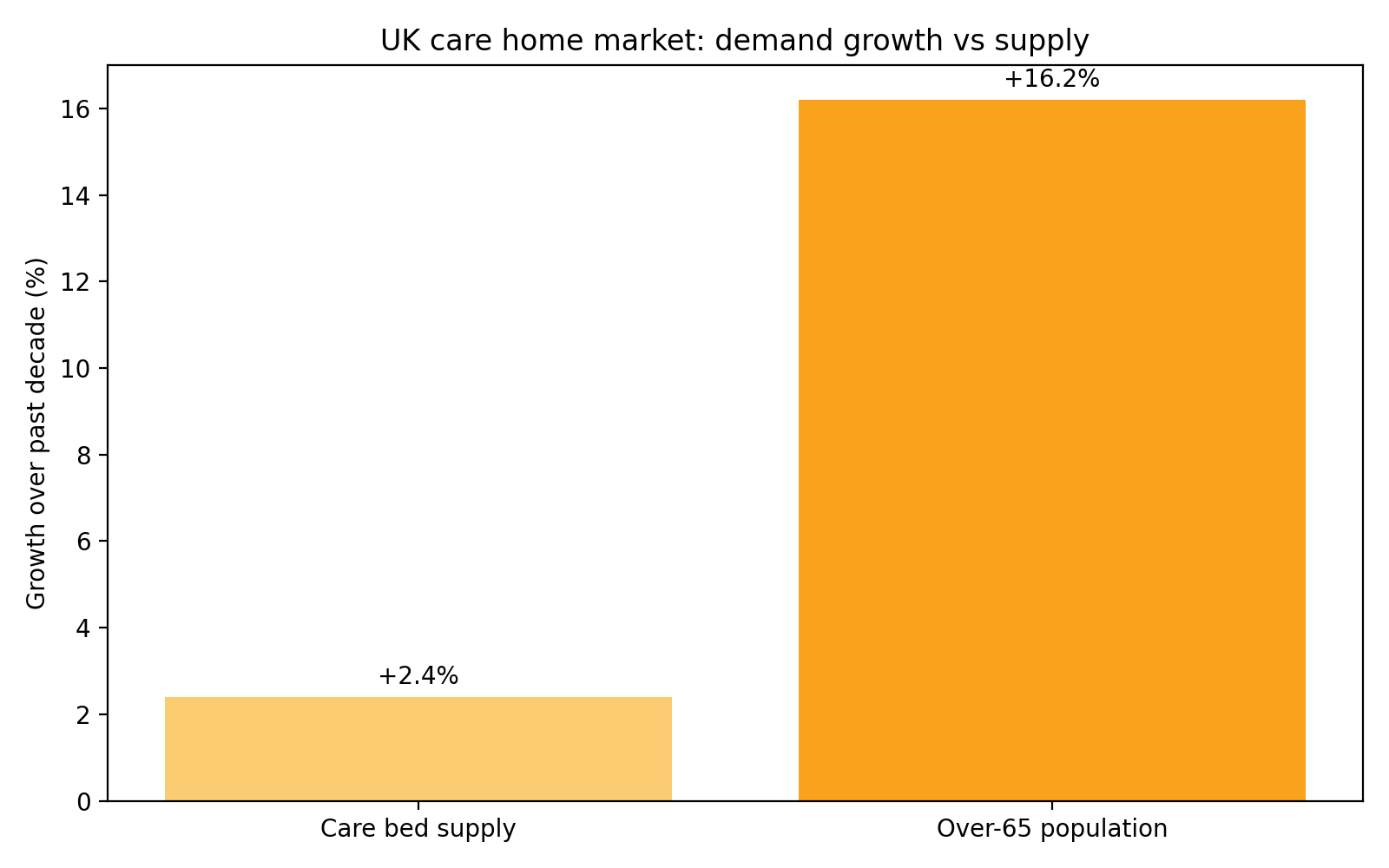

Strong demand alone does not translate into consistent financial performance. Care homes are capital intensive and margin sensitive. Rising labour, energy and financing costs are outpacing fee growth across large parts of the sector, while planning, regulatory and workforce constraints continue to limit deliverable supply. Over the past decade, UK care bed supply has grown by just 2.4%, compared with 16.2% growth in the over-65 population, according to sector data. Net new supply is largely offset by supply leakage and the rising deregistration of older stock.

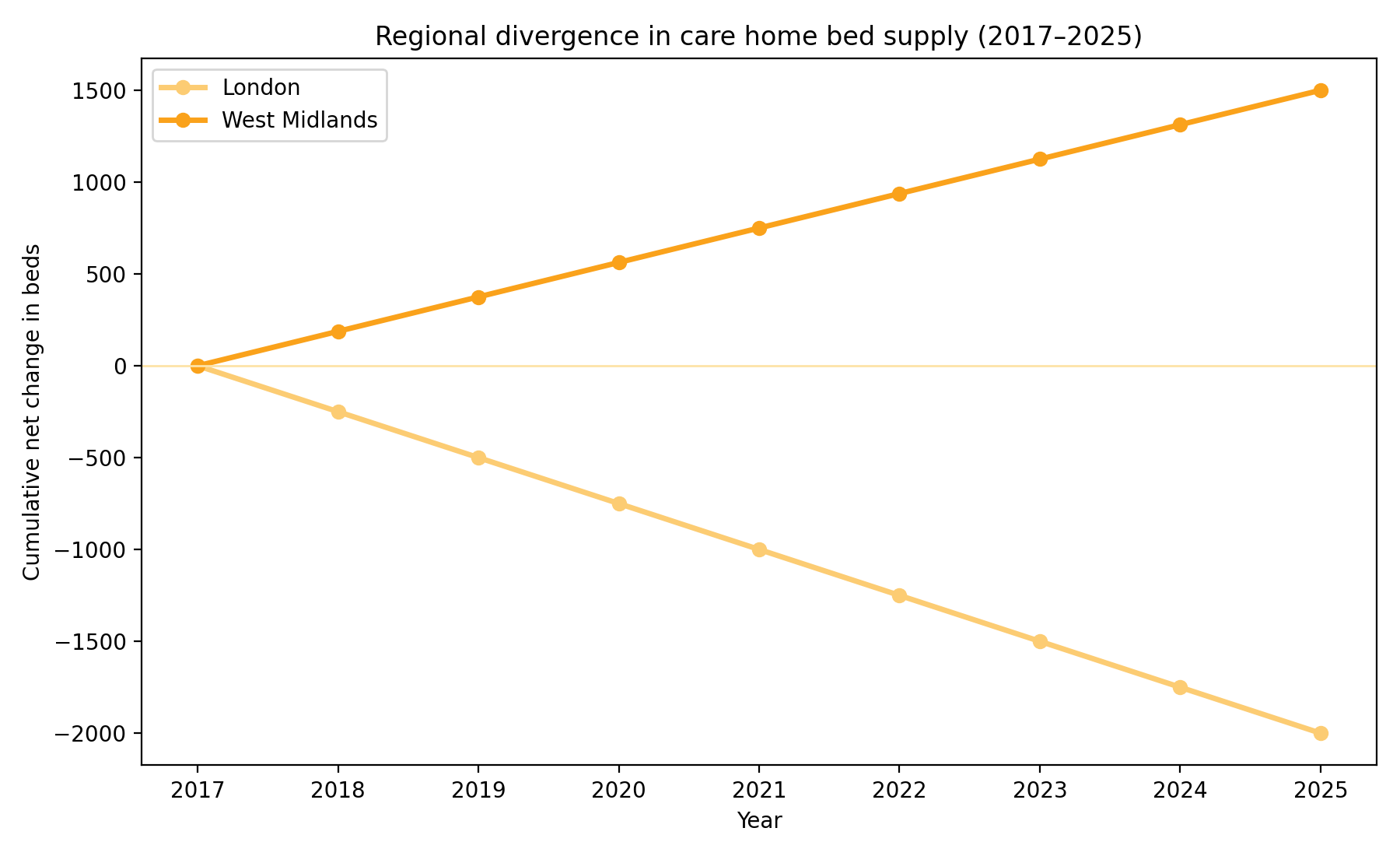

Supply-demand dynamics reveal sharp regional differences in net supply and funding mix. For example, net supply in London declined by around 2,000 beds over 2017 to 2025, compared to a net gain of around 1,500 beds in the West Midlands over the same period. London’s supply leakage is partly offset by its stronger self-funded resident mix, enabling operators to pass through inflation. According to the latest available ONS estimates, self-funders make up around 37% nationally, compared to 49% in the South East.

By contrast, local authority-funded fees continue to lag sharply behind costs. In 2024, average local authority-provided rents increased by 4.5% even as the national living wage (NLW) rose by 10%. When employer national insurance contributions (NICs), energy costs and food inflation are factored in, margin compression becomes more acute, which tends to reveal itself in less affluent UK regions. The result is a bifurcated market, where profitability is primarily determined by funding mix. However, demand is not always fully realised in higher-cost regions as elevated fees and labour constraints can suppress demand, with some households delaying care or substituting with home-based alternatives.

As a result of the above situation, the investment case is increasingly selective. Despite these constraints, the imbalance between structural demand and constrained supply continues to attract significant institutional capital. UK healthcare real estate investment activity exceeded £12bn in 2025, the highest level on record and around four times the five-year prior average, sector data shows. Capital is flowing into the sector, but it is largely deployed into existing platforms and assets rather than to expand capacity, underscoring that it is delivery – not capital – that is the sector’s primary constraint.

Deal activity was led by US Real Estate Investment Trusts (REITs) which tend to trade at a significant premium to their net asset value (NAV), while UK peers often trade at discounts, creating a cost of capital advantage that supports large-scale portfolio acquisitions. US REITs can also utilise RIDEA management contract structures to capitalise directly in operating performance. In October 2025, US REIT Welltower acquired a Barchester operated portfolio of 284 elderly care home assets, including developments, for £5.2bn, and an HC-One operated real estate portfolio for £1.2bn. Both deals were structured with RIDEA management contracts. These transactions highlight international investor appetite for scaled, modern assets where asset management acumen can capture operational upside and portfolios can be acquired at pricing below replacement cost. In addition, the spate of large-scale overseas transactions has reinforced the UK’s position as one of the most attractive care home markets in Europe, supported by its large, resilient self-funded demand base and strong pricing power.

Investors are differentiating more sharply between scalable, well-capitalised operators capable of navigating regulatory complexity and workforce constraints, while smaller and undercapitalised platforms are more exposed to margin compression. Larger operators also tend to better placed to capture demand per asset than smaller providers, supported by strong referral networks and greater brand recognition.

Platform consolidation and sale-and-leaseback structures continue to provide routes to scale and capital recycling. Investment opportunities are concentrated in high-quality, self-funded assets, while a wider cohort of legacy stock and operators faces mounting financial pressures. Capital flowing into the care home sector is gravitating towards newer vintage assets with existing income streams, reinforcing a preference for control and asset management-led value creation over development risk.

© 2026 BTG Consulting plc - Incorporated and registered in England and Wales - VAT Number: 880996072 - Company Registration Number: 05120043

This site uses cookies to monitor site performance and provide a mode responsive and personalised experience. You must agree to our use of certain cookies. For more information on how we use and manage cookies, please read our Privacy Policy.